| Agr723 - 3/7/2024 12:26

RP-HPE is a product that needs to be understood very well before purchasing it.

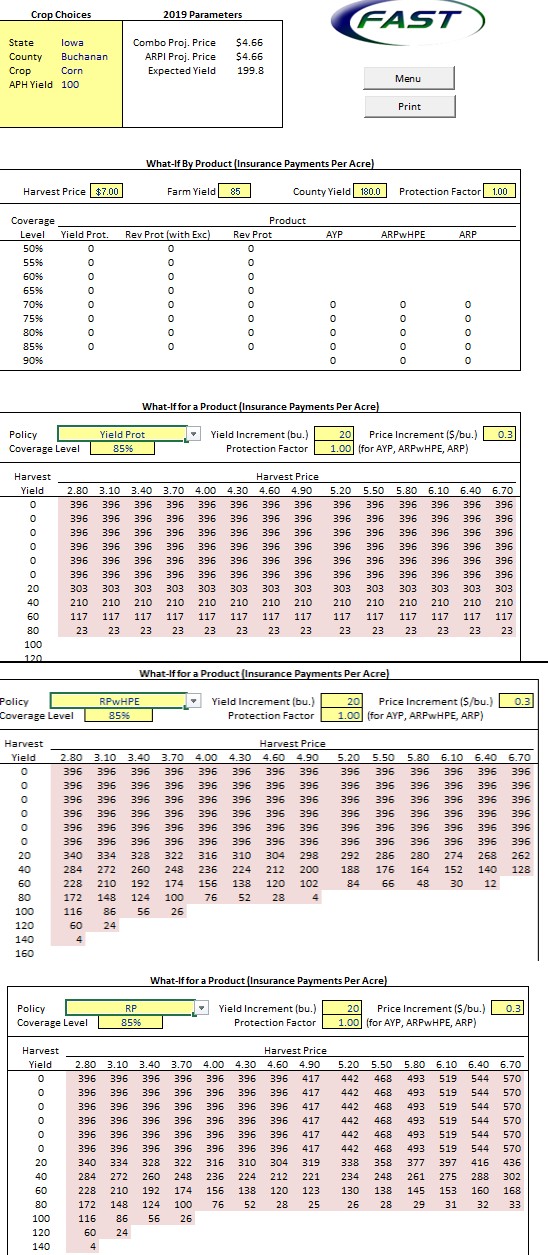

If you are short bushels and the price is higher in the fall than in the spring RP-HPE uses that fall price to determine your revenue so your bushel coverage declines. This can be a real problem with a short crop. For instance on a 100 bushels guarantee at a spring price of $4.66, if the fall price is $7.00 your bushel guarantee drops to 66.5 from 100. If one is absolutely certain the fall price will be lower and has the ability to withstand a lower yield with no insurance coverage if the price goes higher then it works well. If one is going to contract/hedge grain using crop insurance as a risk mitigation tool for that hedge then I would strongly caution against RP-HPE.

Eh. You sound like a salesman to me sorry, if that offends you. In fact, your comments are eerily similar to a guys some years ago about it. Maybe you know him? :-) I take it often and understand the risks very well . If price is 7 dollars, it does not affect his guarantee. You are incorrect. His guarantee is whatever his APH is - less the discount his policy covers, * times the spring price. If he has a short crop, it pays at the spring price if its below his guarantee. Easy figuring, 100 bushel APH at 85% coverage = 85 bushel trigger * 4.66. If he yields 84.9 bushel or less, he will get paid - regardless of what the fall price is. But you won't get the benefit of the higher fall price though. It could suck under the right circumstances sure like a short crop, and heavily sold at lower prices and you can't fill the contracts. But its very hard to be paid by insurance on the revenue side without a yield loss - see comparison. And since he was talking about taking a 60% policy, I am gonna guess he is not to concerned about that or he would be talking taking 85% YP or a higher level of RP - certainly not 60%.

Take care.

Edited by NEIAAG 3/7/2024 13:06

(rma insurance comparison (full).png) (rma insurance comparison (full).png)

Attachments

----------------

rma insurance comparison (full).png (228KB - 21 downloads) rma insurance comparison (full).png (228KB - 21 downloads)

|

How do I determine value of CRC RP vs YP policy

How do I determine value of CRC RP vs YP policy